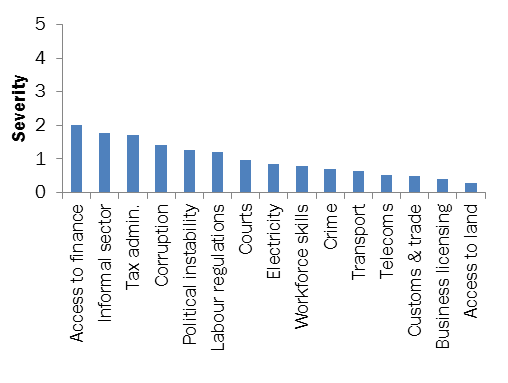

In BEEPS V, the top three business environment obstacles identified by Croatian firms were access to finance; competitors’ practices in the informal sector; and tax administration (Chart 1). The same obstacles were also ranked at the top in BEEPS IV, pointing to little improvement in these areas. Large firms found tax administration to be their biggest struggle, followed by access to finance and labour regulations, while manufacturing firms ranked corruption as the second main constraint.

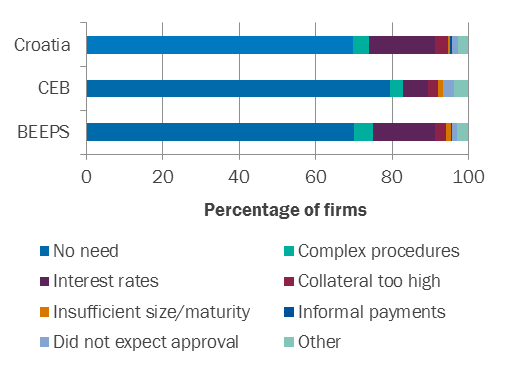

Access to finance emerged as the top obstacle in Croatia. Of the firms surveyed, 29% applied for a loan or a line of credit in BEEPS V and almost 30% of them reported that their application was rejected; nearly double the central Europe and the Baltic states (CEB) average. Of those that did not apply for a loan, 17.3% stated that the reason was high interest rates (Chart 2). Of the firms surveyed, 53.7% had a credit line or a loan, which is above the CEB average of 40.5%. However, more than half of the firms (57.2%) that needed a loan were credit-constrained – they were either discouraged from applying for a loan or rejected when they applied. Croatian firms relied more on bank financing than CEB firms on average: around 18.6% of fixed assets and 9.8% of working capital were financed by bank loans, and the median collateral (as a percentage of loan value) was 173%, well above the CEB median of 153%. In regard to payment, 56.6% of purchases and 61.5% of sales were paid after delivery in BEEPS V, compared with around 51.5% for both in CEB.

In the latest BEEPS round, 48% of firms reported that they competed against unregistered or informal firms – the second highest in CEB after Lithuania. This is a very high percentage, as the CEB average is only 35%, and could be a consequence of the state’s relatively strict labour regulations. Croatia has focused on repressive measures to tackle undeclared work, but has made little use of incentives to encourage those working in the informal sector to formalise. Measures to foster commitment to tax morality are also fairly recent.

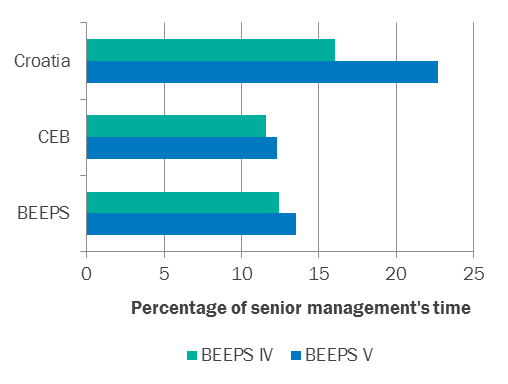

Tax administration was also a major concern. In BEEPS V senior management spent 22.7% (compared with 16% in BEEPS IV) of their time dealing with government regulations, almost twice the CEB average of 11.6% (Chart 3). Of the firms surveyed, 35% were inspected by tax officials in BEEPS V, slightly below the CEB average of 36%. The frequency of inspections by tax officials has not changed significantly since BEEPS IV; it remained at roughly three visits per year.